14 Paying for our renovation

October 2024

OK, it’s time for me to address the elephant in the room. There’s no getting around the fact that this renovation is going to cost us hundreds of thousands of dollars. How the heck will we pay for it?

This chapter talks about money, which is an emotional topic for most people. Decisions about money are highly personal and what worked for us may not work for you.

Nothing you read here should be considered to be financial advice. Talk to an honest-to-god financial planner before making any decisions about spending your hard-earned dollars. Making a mistake here can be very costly.

As an example, if you lose your life savings on Robinhood.com, deleting the app will not bring it back. Get professional help.

All that said, not talking about the money involved in a home renovation would be like not talking about crusts when making a pie. It’s not the most important ingredient in the recipe, but it’s definitely in the top 3, and you’ll have a bad outcome if you mess it up.

OK, I admit it: I’m a boomer.

What that means is that having been born in the 1950s, I started working in the mid-1970s and worked for almost 50 years before I retired. Further, for most of that career, I was both gainfully employed at tech companies and contributed to a variety of retirement vehicles, most of which were tax-deferred. As a result, I have the ability to fund our renovation using my Individual Retirement Account.

Now in discussing our budget, I’m going to employ the This Old House technique of speaking in generalities and never cite absolute amounts we spent (although you’ve already seen the estimates and quotes received, and those are in the ballpark of what we are spending). I will say that we didn’t delude ourselves into thinking we could do this cheaply. I estimated that to achieve our goals, we would have to budget about the same amount we spent to buy our house in 2002 in 2002 dollars (not adjusted for inflation).

What??? Why didn’t you just buy a new house?

Now that you’ve picked up your jaw off the floor, let me explain why this actually makes financial sense.

Yes, we could have sold our existing house and bought a new one. However, if we had done that we would have:

- Had to find a new house in a very competitive housing market. Greater Boston real estate is in high demand with very little supply. It would have been quite difficult to find another house of comparable quality.

- Assured ourselves that it would suit our aging-in-place needs. As noted in my previous post, our goals were to be able to access the entire house even if we were on crutches or in a wheelchair. Further, we wanted to be able to cook, bathe, and otherwise function despite increasingly limited mobility in our later years.

- Had to sell our old house as is or renovate it for sale. While we’re sure we could have sold our existing home at a substantial profit, we still would have had to renovate the kitchens and bathrooms to maximize the sale price. Plus we would have had to make some repairs to the windows and trim that have taken a beating over the last 40 years.

- Lost the gorgeous views that brought us here in the first place. Even if we were to find a new house that allowed aging in place and that we could buy, few would have to near-unique view that we love so much. And besides, as I noted in the first posting of this series, I really hate to move.

Renovation is not money down the drain

If you think education is expensive, try ignorance. —Robert Orben

Corollary: if you think renovation is expensive, try pricing senior living arrangements –Carl Howe

While spending the price of a house for an aging-in-place renovation may seem expensive, we are justifying our renovation costs because:

Senior living costs are high too. We assume that by renovating to age in place, we can avoid moving to an assisted living facility for some number of years. According to the Commonwealth of Massachusetts, the median cost of a 1 to 2 bedroom assisted living facility is between $75,000 and $110,000 per year. If we can remain in our own home for 5 or more years when we otherwise would have had to move to senior care, we could easily cover our budgeted cost while living in a far superior environment.

Renovation adds to the value of our home investment. Rebuilding our home simply changes cash savings into real estate assets. While we don’t expect to recoup our full renovation investment, we do expect it will increase our home value as the result of our changes. Further, we can focus our spending on things that are meaningful to us and that will help us live longer (we hope).

Knowing that we weren’t just throwing our money away made us feel better, but it did lead to an obvious question: how do we pay for it?

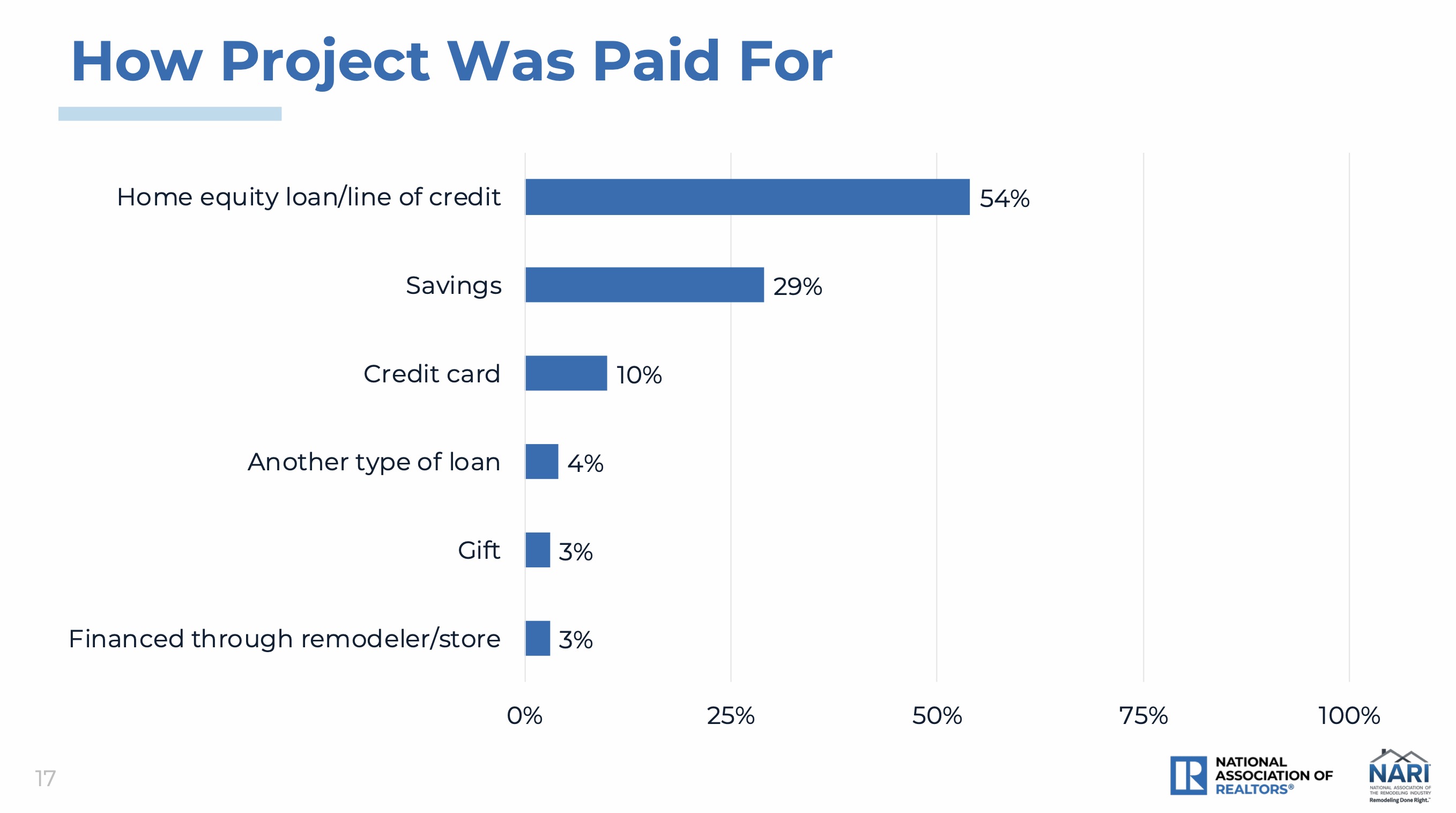

Well, various folks out there have gathered data about this, as shown below:

Survey data from the National Association of Realtors about how homeowners pay for their remodeling projects

Fundamentally, most people choose from three options to pay for a renovation:

Income. If you have six figures worth of free cash flow from your business, investments or job, you might be able to pay for your renovation from that income. This is not a common situation. Most ordinary people who don’t see multiple commas in their income statements have to consider other options.

Assets. Some people have savings, securities, or trust funds they can use to fund a renovation. If this situation applies to you, congratulations! However, you might want to read on to the next section to consider some options other than just spending those assets.

Loans. This is the most common way that home owners fund a renovation. This is usually done through a vehicle called a Home Equity Line of Credit (HELOC), which is essentially a second mortgage and has paperwork requirements to match. Other less-common options include personal loans and credit cards, especially for small projects.

Frankly, the most common financing approach is a combination of all of the above.

I haven’t been too worried about the price of our renovation because I have retirement assets.

I worked for almost 50 years as a software engineer, analyst, and high technology teacher. I started contributing to my retirement starting at age 24 and never stopped, so those funds have had nearly half a century to compound. Add in the fact that I was a big disciple of Peter Lynch’s philosophy of investing1, and the result is that I have a substantial nest egg, almost all of which is in tax-deferred retirement accounts.

1 Peter Lynch was the investment manager of Fidelity’s Magellan Fund for 13 years. He guided that fund to a nearly 30% annual return, making it the best performing mutual fund in the world. In his 1994 book Beating the Street, Lynch recounts teaching a group of 7th graders at St. Agnes his strategies for investing. The paper portfolio created by those 7th graders achieved a 70% return over a two-year period, outperforming the S&P 500 composite and 99% of all equity mutual funds, proving you don’t need an MBA or a Bloomberg terminal to do well at investing.

Now the fact that these assets are in retirement accounts actually creates two new problems to work around.

- Tax-deferred retirement accounts can’t be used for loans. It would have been nice to just take a loan out against my retirement assets, but the IRS explicitly prohibits this.

- Withdrawing retirement funds triggers taxes. Actually withdrawing the retirement funds to cover the renovation would incur very high federal and Massachusetts income tax liabilities in the year in which the withdrawal occurred.

A fourth option: spread out withdrawals using a loan

When we starting getting serious about our project, I met with our financial advisor. He noted that because our project is likely to extend from 2024 through 2025, we could do a bit of planning that would save us substantial amounts of tax. The plan goes like this:

- Year 1: Withdraw about half of the project amount. This allows us to pay for the initial deposit while still keeping us below the highest tax brackets. It also leaves us with some liquid cash to make payments in year 2.

- Year 2: Take out a line of credit while withdrawing another third. The line of credit is backed by assets we have on hand, so it carries a low interest rate. This combined with some additional withdrawals allows us to pay for the majority of the work. And because the loan is not income, the money we borrow isn’t taxed. Further, unlike with a mortgage, the only payments we make on the loan are for interest.

- Year 3: Make final withdrawals to pay off the loan and any residual bills. The final withdrawals from the retirement accounts allow us to pay off the principal of the loan while still keeping us out of the highest tax brackets.

I normally am not a fan of fancy financial engineering to avoid taxes. However, given the high cost of the renovation we’re planning, I think this plan is worthwhile.

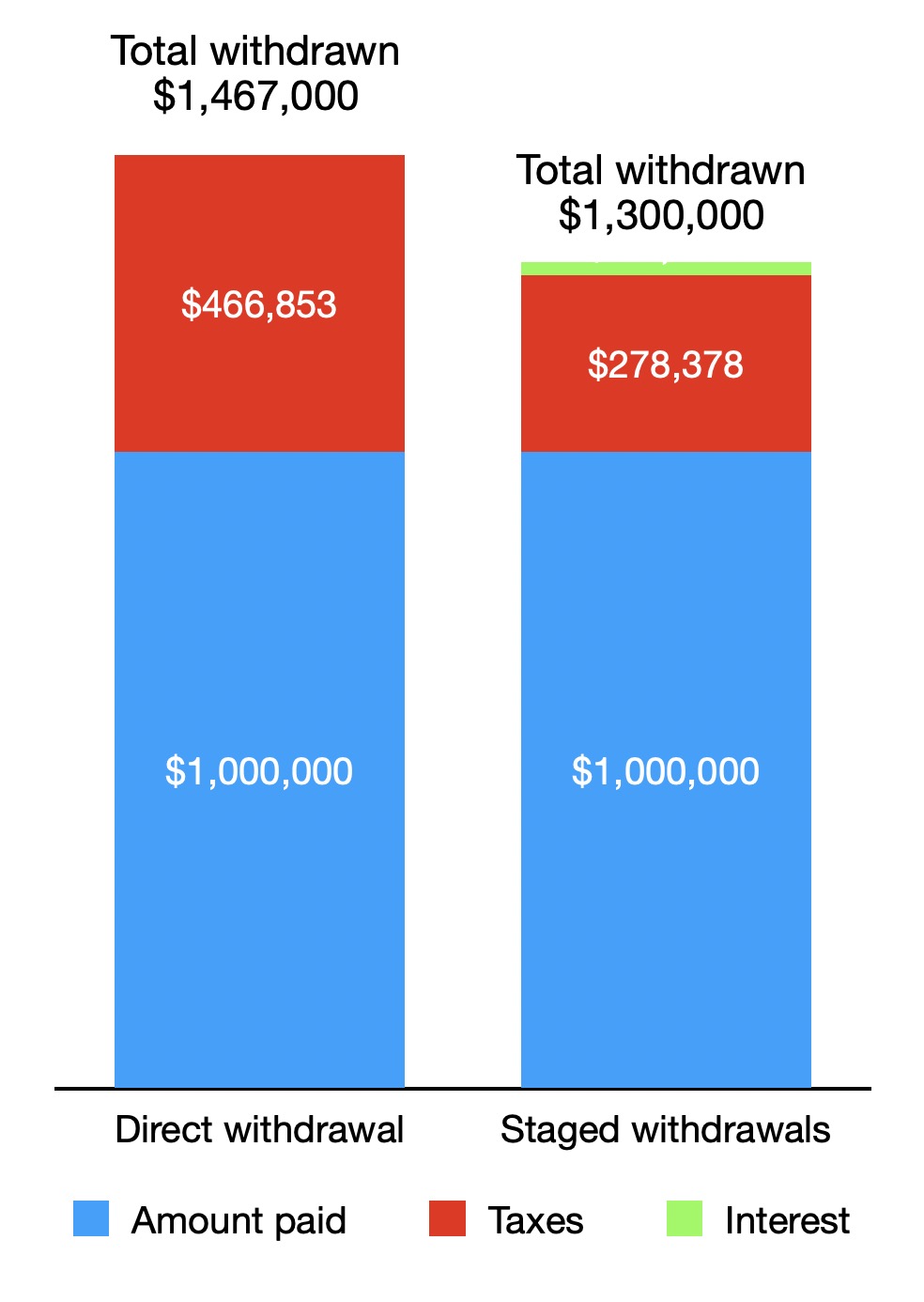

Using round numbers for illustration, let’s assume we need to pay $1 million for our renovation. To withdraw enough retirement funds to pay the contractor $1 million, we’d have to withdraw $1,467,000 to pay the $467,000 in taxes because much of that amount would be taxed at the maximum tax rate of 38%.2 However, by spreading out the tax burden over 3 years, the taxes for each year average only $93,000 because we never hit the top two tax brackets.

2 That $467,000 number I calculated is based on the 2025 tax tables for a married couple filing jointly without any other income. Since we also need money to live on, the actual figure will be higher. Regardless, the savings are significant.

As shown in the chart above, I calculate that spreading the cost of this hypothetical renovation out over 3 years will save us about $187,000 in income taxes overall. We will have to pay about $20,000 in interest on the loan (actually a bit less because we don’t withdraw against the line of credit all at once), but we still end up saving about $167,000 in taxes. It really is worth doing.